by JON PRIOR

Foreclosure filings increased from last year in 133 of 206 metropolitan statistical areas tracked in the third quarter, or 65%, according to RealtyTrac.

The Seattle area had the highest increase. There, foreclosure filings, which include notices of default, pending cases, notices of foreclosure sale and repossessions, increased 71% from the third quarter of 2009. Chicago was second with a 35% increase followed by Houston, Texas at 26%.

California, Florida, Nevada and Arizona accounted for 19 of the top-20 foreclosure rates in the country. The only exception was Boise City, Idaho, which was 14th.

Las Vegas posted the highest rate in the third quarter, where one in every 25 housing units received a filing, more than five times the national average. The 32,288 filings is down 20% from last year.

Cape Coral-Fort Meyers, Fla. was second with a one in 35 foreclosure rate. Filings there reached 10,352, down 22%. One in 36 houses in Modesto, Calif. received a filing in the third quarter for the third highest rate, but it was an 18% drop from a year ago.

Miami, Fla. posted the highest total number of foreclosures in the third quarter, at more than 58,600 filings. It's an increase of 9% from last year and up 25% from the previous quarter.

“The underlying problems that are causing homeowners to miss their mortgage payments — high unemployment, underemployment, toxic loans and negative equity — are continuing to plague most local housing markets,” said James Saccacio, CEO of RealtyTrac. “And these historically high foreclosure rates will continue until those problems are resolved.”

URL to original article: http://www.housingwire.com/2010/10/28/foreclosures-increase-in-65-of-msas-in-3q-realtytrac

Sunday, October 31, 2010

Friday, October 29, 2010

The Real Estate Market and New Sales Agents

Just wanted to let everyone know that the Real Estate Market is very active right now. I'm so happy that the month of October has been very busy and that I see our London Agents making things happen.

I also wanted to welcome aboard these new sales agent; Brandy Tschappler, Brandy come to us from New Homes, Kellie Matina formerly of ERA Power Properties in Hanford, Erik Abram formerly of Chapman Real Estate, Linda Navarro formerly of Docter & Docter R. E., Tammy Katuin & Kathy Patterson formerly of The R.E. Network, Phillip Frias formerly of All State Homes. Welcome

I also wanted to welcome the follow new agents to the business. These people have passed their Real Estate License exam in October. Tammy Burgess working out of Merced office, Jasmin Goncalves also working out of our Merced office, Anthony Bishop will be working in our Fresno office, Brain Jensen also working out of our Fresno office, Harlan Garcia will be working out of our Kingsburg office, Chris Horton & Conner Herring will be working out of Fresno office and Ray Lopez he will be working out of our Clovis office.

Welcome aboard to all of you and go get'em!!!

I also wanted to welcome aboard these new sales agent; Brandy Tschappler, Brandy come to us from New Homes, Kellie Matina formerly of ERA Power Properties in Hanford, Erik Abram formerly of Chapman Real Estate, Linda Navarro formerly of Docter & Docter R. E., Tammy Katuin & Kathy Patterson formerly of The R.E. Network, Phillip Frias formerly of All State Homes. Welcome

I also wanted to welcome the follow new agents to the business. These people have passed their Real Estate License exam in October. Tammy Burgess working out of Merced office, Jasmin Goncalves also working out of our Merced office, Anthony Bishop will be working in our Fresno office, Brain Jensen also working out of our Fresno office, Harlan Garcia will be working out of our Kingsburg office, Chris Horton & Conner Herring will be working out of Fresno office and Ray Lopez he will be working out of our Clovis office.

Welcome aboard to all of you and go get'em!!!

Thursday, October 28, 2010

Markets' 'liquid courage' sapped

Source: Barrons

LIQUID COURAGE. If you're not acquainted with the term, or more improbably never experienced it, it is the lowering of inhibitions from the consumption of alcohol that allows one to approach strangers you find attractive or confront others whom you think have threatened or insulted you.

At the time, your actions seem reasonable, even suave in the former instance or justified in the latter. Only later, when the euphoric effects of the source of the liquid courage have worn off, does the stupidity of your bravado become evident to you (although it was apparent to everyone else.)

Besides the hangover, the after-effects of the ill-advised encounters will be all too obvious. Brawls leave cuts and bruises while boozy assignations result in worse regrets. As the country song of some years back (well before political correctness) sums them up, "I've never gone to bed with an ugly woman, but I've sure woke up with a few."

For the past two months, global markets have rallied on the courage of the liquidity they expect to come pouring forth after the two-day meeting of the Federal Open Market Committee next Tuesday and Wednesday. Since Fed Chairman Ben Bernanke began suggesting in his speech in Jackson Hole, Wyo., that additional monetary stimulus may be needed to stave off deflation and lower stubbornly high unemployment, so-called risk markets have rallied, adding about $1.7 trillion to the wealth of holders of U.S. stocks.

That inflation of asset values was based on expectations of QE2, the second phase of quantitative easing consisting of the purchase of, coincidentally enough, of $1.7 trillion of Treasury, agency and agency mortgage-backed securities, embarked upon in March 2009. Expectations of the size of QE2 have ranged as high as $2 trillion, as suggested by Goldman Sachs' economists over the weekend, to a virtual regatta of smaller vessels, consisting of a few hundred billion at a time.

The latter seems to be tack that the skippers at the Fed have chosen for QE2. According to Wednesday's Wall Street Journal the central bank appears to have settled on a compromise of several hundred billions of dollars in Treasury purchases, a middle ground between those calling for a trillion-dollar-plus buy and those who want nothing.

As I pointed out in the print edition of this column in this week's Barron's while the anticipated influx of liquidity had boosted the stock market, it simultaneously had the offsetting effects of driving down the dollar and sending commodity prices jumping. The 13% spurt in the Standard & Poor's 500 since late August has been nearly matched by the rise in the price that I'm paying at the gasoline pump.

Moreover, in just one of the perceptive, indeed searing, observations made by Jeremy Grantham—the "G" in GMO, the highly regarded institutional money manager—in his most recent investment commentary, ultra-low interest rates may provide no stimulus whatsoever to the economy. The loss of income to retirees, who need it, offsets the benefits to big corporations, which don't need the ability to borrow cheaply. (To get the full scope of Grantham's scathing assessment of Fed monetary manipulation, go to www.gmo.com.)

Moreover, QE2 (or the anticipation of its arrival) has ceased to produce its intended effect—a reduction in bond yields. Observes Uwe Parpart, Cantor Fitzgerald's keen-eyed Asia strategist, the Treasury 10-year note yield has increased to 2.72% from 2.33% on Oct. 8. "What the bond market is tell the Fed is: you can't have it both ways, on one hand ramping up QE and wishing for higher inflation and at the same time wanting rates to stay ultra-low," he writes in a note to clients Wednesday.

With the Fed likely to dump less hooch in the monetary punchbowl, risk markets reversed course Wednesday. The stock market ran into resistance right at its April highs while bonds continue to slump but the dollar's slide paused, as Barrons.com technical guru, Michael Kahn, points out in his Getting Technical column.

Bartender Ben Bernanke may not be pouring as generously as the slightly tipsy markets had been hoping. The markets may thank him the next morning.

URL to original article: http://www.housingwire.com/2010/10/28/markets-liquid-courage-sapped

LIQUID COURAGE. If you're not acquainted with the term, or more improbably never experienced it, it is the lowering of inhibitions from the consumption of alcohol that allows one to approach strangers you find attractive or confront others whom you think have threatened or insulted you.

At the time, your actions seem reasonable, even suave in the former instance or justified in the latter. Only later, when the euphoric effects of the source of the liquid courage have worn off, does the stupidity of your bravado become evident to you (although it was apparent to everyone else.)

Besides the hangover, the after-effects of the ill-advised encounters will be all too obvious. Brawls leave cuts and bruises while boozy assignations result in worse regrets. As the country song of some years back (well before political correctness) sums them up, "I've never gone to bed with an ugly woman, but I've sure woke up with a few."

For the past two months, global markets have rallied on the courage of the liquidity they expect to come pouring forth after the two-day meeting of the Federal Open Market Committee next Tuesday and Wednesday. Since Fed Chairman Ben Bernanke began suggesting in his speech in Jackson Hole, Wyo., that additional monetary stimulus may be needed to stave off deflation and lower stubbornly high unemployment, so-called risk markets have rallied, adding about $1.7 trillion to the wealth of holders of U.S. stocks.

That inflation of asset values was based on expectations of QE2, the second phase of quantitative easing consisting of the purchase of, coincidentally enough, of $1.7 trillion of Treasury, agency and agency mortgage-backed securities, embarked upon in March 2009. Expectations of the size of QE2 have ranged as high as $2 trillion, as suggested by Goldman Sachs' economists over the weekend, to a virtual regatta of smaller vessels, consisting of a few hundred billion at a time.

The latter seems to be tack that the skippers at the Fed have chosen for QE2. According to Wednesday's Wall Street Journal the central bank appears to have settled on a compromise of several hundred billions of dollars in Treasury purchases, a middle ground between those calling for a trillion-dollar-plus buy and those who want nothing.

As I pointed out in the print edition of this column in this week's Barron's while the anticipated influx of liquidity had boosted the stock market, it simultaneously had the offsetting effects of driving down the dollar and sending commodity prices jumping. The 13% spurt in the Standard & Poor's 500 since late August has been nearly matched by the rise in the price that I'm paying at the gasoline pump.

Moreover, in just one of the perceptive, indeed searing, observations made by Jeremy Grantham—the "G" in GMO, the highly regarded institutional money manager—in his most recent investment commentary, ultra-low interest rates may provide no stimulus whatsoever to the economy. The loss of income to retirees, who need it, offsets the benefits to big corporations, which don't need the ability to borrow cheaply. (To get the full scope of Grantham's scathing assessment of Fed monetary manipulation, go to www.gmo.com.)

Moreover, QE2 (or the anticipation of its arrival) has ceased to produce its intended effect—a reduction in bond yields. Observes Uwe Parpart, Cantor Fitzgerald's keen-eyed Asia strategist, the Treasury 10-year note yield has increased to 2.72% from 2.33% on Oct. 8. "What the bond market is tell the Fed is: you can't have it both ways, on one hand ramping up QE and wishing for higher inflation and at the same time wanting rates to stay ultra-low," he writes in a note to clients Wednesday.

With the Fed likely to dump less hooch in the monetary punchbowl, risk markets reversed course Wednesday. The stock market ran into resistance right at its April highs while bonds continue to slump but the dollar's slide paused, as Barrons.com technical guru, Michael Kahn, points out in his Getting Technical column.

Bartender Ben Bernanke may not be pouring as generously as the slightly tipsy markets had been hoping. The markets may thank him the next morning.

URL to original article: http://www.housingwire.com/2010/10/28/markets-liquid-courage-sapped

The government’s incredible shrinking mortgage mod program

Source: ProPublica

The U.S. government's effort to help struggling homeowners is approaching a standstill, and the number of homeowners in ongoing mortgage modifications could start shrinking in several months if current trends continue, according to a ProPublica analysis of Treasury Department data.

A year and a half into the program, the number of homeowners defaulting on their modified loans has been fast approaching the number of new modifications. In September, for example, banks modified almost 28,000 loans, but nearly 10,000 homeowners fell out of the program because they defaulted on their modified payments. Taken together, the programs' growth has slowed by almost a quarter each month since May.

The administration launched its foreclosure-relief effort last spring, looking to help 3 to 4 million homeowners by modifying their mortgages to have affordable monthly payments. Only 467,000 homeowners are in modifications that are still ongoing.

URL to original article: http://www.housingwire.com/2010/10/27/the-government%e2%80%99s-incredible-shrinking-mortgage-mod-program

The U.S. government's effort to help struggling homeowners is approaching a standstill, and the number of homeowners in ongoing mortgage modifications could start shrinking in several months if current trends continue, according to a ProPublica analysis of Treasury Department data.

A year and a half into the program, the number of homeowners defaulting on their modified loans has been fast approaching the number of new modifications. In September, for example, banks modified almost 28,000 loans, but nearly 10,000 homeowners fell out of the program because they defaulted on their modified payments. Taken together, the programs' growth has slowed by almost a quarter each month since May.

The administration launched its foreclosure-relief effort last spring, looking to help 3 to 4 million homeowners by modifying their mortgages to have affordable monthly payments. Only 467,000 homeowners are in modifications that are still ongoing.

Alan White, a law professor at Valparaiso University, said the problem isn't the rate at which homeowners are redefaulting, which is low compared to other modifications, but rather the shrinking number of new modifications given out by banks. "We need to be modifying 10 times as many a month," he told us.

Across the country, over 5 million mortgages are more than 60 days overdue or in foreclosure, according to Lender Processing Services.

Banks have had a poor record of modifying mortgages under the government program. (Check out our graphical breakdown of each bank's performance.) Homeowners report Kafka-esque experiences of lost paperwork, miscommunication and dashed hopes in trying to get help preventing foreclosures. We've recently chronicled homeowner experiences in a series of profiles and a questionnaire. Investors who own mortgages are dismayed as well. The Treasury Department has yet to penalize a single mortgage servicer since the program launched last spring.

"You start with a program that's not well designed and a lack of will to enforce the program, and this is what you're getting," says White.

The pipeline for permanent modifications also continues to dwindle. There are now fewer than 175,000 active trial modifications, down from almost 260,000 in July. Nearly half of the active trials are at least six months old.

We contacted Treasury to ask about the slowing of the program, and they haven’t responded yet. We'll update this post when we hear back.

Two mortgage servicers, Bank of America and Aurora, have seen their numbers of active permanent modifications decrease in the past month. Bank of America's dropped by about a thousand modifications, and Aurora's fell by over 2,500 modifications.

In a press release, Bank of America said that the drop came from a combination of defaulted modifications, servicing transfers and repaid mortgages. Only 428 mortgages have been repaid to the more than 100 mortgage servicers participating in the federal program. Aurora did not respond to ProPublica's request to comment.

Update: Treasury said it is working to reach as many eligible homeowners as it can and has expanded alternative options for borrowers that do not qualify for the modification program.

URL to original article: http://www.housingwire.com/2010/10/27/the-government%e2%80%99s-incredible-shrinking-mortgage-mod-program

Wednesday, October 27, 2010

Real house prices, price-to-rent ratio

Source: Calculated Risk

URL to original article: http://www.housingwire.com/2010/10/26/real-house-prices-price-to-rent-ratio

Yesterday CoreLogic reported that house prices declined 1.2% in August, and this morning S&P Case-Shiller reported widespread price declines in August (really an average of June, July and August).

Click on graph for larger image in new window.

This post looks at real prices and the price-to-rent ratio, but first here is a graph of the two Case-Shiller composite indexes, and the CoreLogic HPI (NSA).

All three indexes are above the lows of early 2009, but it appears that prices are now falling - and I expect all three indexes to show new lows later this year or in early 2011.

Price-to-Rent

In October 2004, Fed economist John Krainer and researcher Chishen Wei wrote a Fed letter on price to rent ratios: House Prices and Fundamental Value. Kainer and Wei presented a price-to-rent ratio using the OFHEO house price index and the Owners' Equivalent Rent (OER) from the BLS. Here is a similar graph through August 2010 using the Case-Shiller Composite 20 and CoreLogic House Price Index.

Here is a similar graph through August 2010 using the Case-Shiller Composite 20 and CoreLogic House Price Index.

This graph shows the price to rent ratio (January 1998 = 1.0).

Recent reports suggest rents might have bottomed, but this suggests that house prices are still a little too high on a national basis.

Real House Prices The third graph shows the CoreLogic house price index and the Case-Shiller Composite 20 index through August 2010 in real terms (adjusted with CPI less Shelter).

The third graph shows the CoreLogic house price index and the Case-Shiller Composite 20 index through August 2010 in real terms (adjusted with CPI less Shelter).

These indexes are still above the 2009 lows in real terms, but it is getting close, and I expect new real price lows sometime in the next few months.

This isn't like in 2005 when prices were way out of the normal range by these measures, but it does appear prices are still a little too high. And with high levels of inventory, prices will probably fall some more.

URL to original article: http://www.housingwire.com/2010/10/26/real-house-prices-price-to-rent-ratio

Tuesday, October 26, 2010

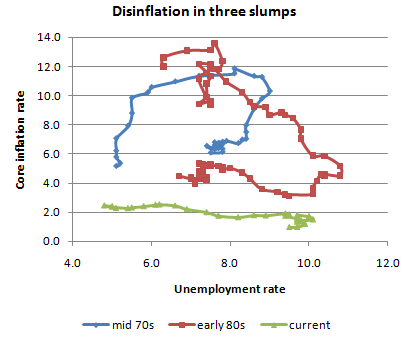

Do investors expect too much from Bernanke?

Source: The New York Times

The 5-year TIPS spread

The 5-year TIPS spread

URL to original article: http://www.housingwire.com/2010/10/26/do-investors-expect-too-much-from-bernanke

Do Investors Expect Too Much From Bernanke?

Financial markets seem convinced that quantitative easing will be highly effective at solving at least one problem: inflation running well below the Fed’s 2-percent-or-so target. The chart above shows the difference between interest rates on 5-year inflation-protected bonds (which are now negative) and rates on unprotected bonds; implicitly, the market forecast of inflation over the next five years has risen half a point.

But I really don’t understand this. Granted that QE2 will probably have some positive effect, hopefully bigger than analysis based on the debt-maturity equivalence suggests. Still, the prospect remains that we’ll face multiple years of high unemployment — or, if you prefer, a protracted large output gap (PLOG). And history is clear on what that means: declining inflation:

My guess, then, is that the markets are overreacting; they’re thinking, “The Fed is printing money!”, while forgetting that this ultimately matters, even for inflation, only to the extent that it seriously reduces unemployment.

URL to original article: http://www.housingwire.com/2010/10/26/do-investors-expect-too-much-from-bernanke

Obama housing scorecard: Market fragile with signs of stabilization

by KERRY CURRY

The U.S. housing market remains fragile but is showing some signs of stabilization, according to the Obama administration's 2010 October housing scorecard.

Rates for 30-year, fixed-rate mortgages remain at all-time lows, helping 7.1 million homeowners refinance since April 2009 and resulting in $12.7 billion in homeowner savings, the scorecard noted.

On the minus side, home sales have declined with the expiration of the homebuyer tax credit, although home prices have shown some indication of stabilization.

The Department of Housing and Urban Development and the Treasury Department compiled data for the monthly scorecard.

More than 3.52 million modification arrangements were started between April 2009 and the end of August 2010 — nearly triple the number of foreclosure completions during that time. These included more than 1.3 million trial Home Affordable Modification Program starts, more than 510,000 Federal Housing Administration loss-mitigation and early-delinquency interventions, and more than 1.6 million proprietary modifications under HOPE Now.

At nine months, almost 90% of homeowners remain in their permanent HAMP modification, with 11% defaulted, according to the data.

The scorecard shows that the number of existing homes on the market is below its 2008 peak, but data indicate that the number of units held off the market is on the rise.

Data in the scorecard also show that the recovery in the housing market continues to be tepid.

"Foreclosure completions continue to move upward and a large supply of homes are being held off the market," the scorecard notes. "While the recovery will take place over time, the administration remains committed to its efforts to prevent avoidable foreclosures and stabilize the housing market."

URL to original article: http://www.housingwire.com/2010/10/25/obama-housing-scorecard-market-fragile-with-signs-of-stabilization

The U.S. housing market remains fragile but is showing some signs of stabilization, according to the Obama administration's 2010 October housing scorecard.

Rates for 30-year, fixed-rate mortgages remain at all-time lows, helping 7.1 million homeowners refinance since April 2009 and resulting in $12.7 billion in homeowner savings, the scorecard noted.

On the minus side, home sales have declined with the expiration of the homebuyer tax credit, although home prices have shown some indication of stabilization.

The Department of Housing and Urban Development and the Treasury Department compiled data for the monthly scorecard.

More than 3.52 million modification arrangements were started between April 2009 and the end of August 2010 — nearly triple the number of foreclosure completions during that time. These included more than 1.3 million trial Home Affordable Modification Program starts, more than 510,000 Federal Housing Administration loss-mitigation and early-delinquency interventions, and more than 1.6 million proprietary modifications under HOPE Now.

At nine months, almost 90% of homeowners remain in their permanent HAMP modification, with 11% defaulted, according to the data.

The scorecard shows that the number of existing homes on the market is below its 2008 peak, but data indicate that the number of units held off the market is on the rise.

Data in the scorecard also show that the recovery in the housing market continues to be tepid.

"Foreclosure completions continue to move upward and a large supply of homes are being held off the market," the scorecard notes. "While the recovery will take place over time, the administration remains committed to its efforts to prevent avoidable foreclosures and stabilize the housing market."

URL to original article: http://www.housingwire.com/2010/10/25/obama-housing-scorecard-market-fragile-with-signs-of-stabilization

Monday, October 25, 2010

Financial system trust down with Dodd-Frank dissatisfaction

by CHRISTINE RICCIARDI

Trust in the financial system and real estate market is gradually depleting, according to the Chicago Booth/Kellogg School Financial Trust Index results. The survey found trust index to be 25% for the third quarter of 2010, a 1% drop from from the all-time high in June.

The Financial Trust Index is a quarterly survey conducted by Social Science Research Solutions, a branch of AUS and ICR/International Communications Research. The results come from 1,005 phone interviews nationwide.

The authors of the report, both business professors, attribute the lack of trust in the financial industry to the passage of Dodd-Frank, saying that the bill did not meet consumer expectations with regard to reform. The survey found that only 12% of respondents are satisfied with the Dodd-Frank Act while 54% are dissatisfied.

“A primary consequence of the 2008 financial crisis was a large drop in trust Americans had in financial institutions, and we’re seeing a continued decline despite reform enacted to combat this sentiment,” said Paola Sapienza, a professor of finance at the Kellogg School of Management at Northwestern University. “Interestingly, Americans who declared themselves satisfied with the Dodd-Frank Bill trust banks 8% more, but unfortunately only a minority is happy with the legislation.”

Americans trust every sector of the financial system less than they did last quarter except for banks. The percentage of people that trust banks rose to 43% from 39% last quarter.

According to the data, 14% of Americans trust the stock market, down from 18% last quarter; 28% of Americans trust mutual funds, down from 32% in June; and 14% of people trust large corporations, down from 17% last quarter. This is the lowest the index has been for the stock market and mutual fund sector. Only 13% of Americans trusted large corporations in March.

For the first time this year, the majority of homeowners expect home prices in their neighborhood to drop over the next 12 months. Approximately 30% expect a decrease, up from 20% in June and 21% in March. Twenty-three percent of homeowners expect an increase in home prices, down from 26% in June and 31% in March.

URL to original article: http://www.housingwire.com/2010/10/22/financial-system-trust-down-with-dodd-frank-dissatisfaction

Trust in the financial system and real estate market is gradually depleting, according to the Chicago Booth/Kellogg School Financial Trust Index results. The survey found trust index to be 25% for the third quarter of 2010, a 1% drop from from the all-time high in June.

The Financial Trust Index is a quarterly survey conducted by Social Science Research Solutions, a branch of AUS and ICR/International Communications Research. The results come from 1,005 phone interviews nationwide.

The authors of the report, both business professors, attribute the lack of trust in the financial industry to the passage of Dodd-Frank, saying that the bill did not meet consumer expectations with regard to reform. The survey found that only 12% of respondents are satisfied with the Dodd-Frank Act while 54% are dissatisfied.

“A primary consequence of the 2008 financial crisis was a large drop in trust Americans had in financial institutions, and we’re seeing a continued decline despite reform enacted to combat this sentiment,” said Paola Sapienza, a professor of finance at the Kellogg School of Management at Northwestern University. “Interestingly, Americans who declared themselves satisfied with the Dodd-Frank Bill trust banks 8% more, but unfortunately only a minority is happy with the legislation.”

Americans trust every sector of the financial system less than they did last quarter except for banks. The percentage of people that trust banks rose to 43% from 39% last quarter.

According to the data, 14% of Americans trust the stock market, down from 18% last quarter; 28% of Americans trust mutual funds, down from 32% in June; and 14% of people trust large corporations, down from 17% last quarter. This is the lowest the index has been for the stock market and mutual fund sector. Only 13% of Americans trusted large corporations in March.

For the first time this year, the majority of homeowners expect home prices in their neighborhood to drop over the next 12 months. Approximately 30% expect a decrease, up from 20% in June and 21% in March. Twenty-three percent of homeowners expect an increase in home prices, down from 26% in June and 31% in March.

URL to original article: http://www.housingwire.com/2010/10/22/financial-system-trust-down-with-dodd-frank-dissatisfaction

Friday, October 22, 2010

California home sales drop 17% in September: DataQuick

by JON PRIOR

California new and existing home sales totaled 33,176 in September, down 17.5% from a year ago and 3.1% from the previous month, according to the San Diego-based real estate provider DataQuick.

Despite record low mortgage rates, the entire housing market is still waiting for new demand to replace the boost from the homebuyer tax credit that expired in April.

While transactions are down, prices are still up for the 11th month in a row, following more than two years of straight declines.

The median price on a California home was $265,000, a 5.6% increase from last year and a 1.9% bump from the previous month. The trough came in April 2009 at $221,000. The peak was $484,000 in early 2007.

Of the existing home sales completed in September, 35.8% were properties that had been foreclosed on in the last year, down from 41.7% a year ago and flat from the previous month. Foreclosure accounted for more than 58% of the market in February 2009, the all-time high.

Homeowners made an average $1,055 monthly payment in September, down more than 60% from the peak in June 2006.

URL to original article: http://www.housingwire.com/2010/10/21/california-home-sales-drop-17-in-september-dataquick

California new and existing home sales totaled 33,176 in September, down 17.5% from a year ago and 3.1% from the previous month, according to the San Diego-based real estate provider DataQuick.

Despite record low mortgage rates, the entire housing market is still waiting for new demand to replace the boost from the homebuyer tax credit that expired in April.

While transactions are down, prices are still up for the 11th month in a row, following more than two years of straight declines.

The median price on a California home was $265,000, a 5.6% increase from last year and a 1.9% bump from the previous month. The trough came in April 2009 at $221,000. The peak was $484,000 in early 2007.

Of the existing home sales completed in September, 35.8% were properties that had been foreclosed on in the last year, down from 41.7% a year ago and flat from the previous month. Foreclosure accounted for more than 58% of the market in February 2009, the all-time high.

Homeowners made an average $1,055 monthly payment in September, down more than 60% from the peak in June 2006.

URL to original article: http://www.housingwire.com/2010/10/21/california-home-sales-drop-17-in-september-dataquick

How Joseph Lents dodged foreclosure for eight years and started a movement

Source: Bloomberg

In 2002, an accountant in Boca Raton, Florida, named Joseph Lents was accused of securities-law violations by the U.S. Securities and Exchange Commission. Lents, who was chief executive officer of a now-defunct voice- recognition software company, had sold shares in the public company without filing the proper forms. Facing a little over $100,000 in fines and fees, and with his assets frozen by the SEC, Lents stopped making payments on his $1.5 million mortgage.

The loan servicer, Washington Mutual Inc., tried to foreclose on his home in 2003 but was never able to produce Lents’s promissory note, so the state circuit court for Palm Beach County dismissed the case. Next, the buyer of the loan, DLJ Mortgage Capital, stepped in with another foreclosure proceeding. DLJ claimed to have lost the promissory note in interoffice mail. Lents was dubious.

“When you say you lose a $1.5 million negotiable instrument -- that doesn’t happen,” he said in an interview in Bloomberg Businessweek’s Oct. 25 issue.

DLJ claimed that its word was as good as paper. But at least in Palm Beach County, paper still rules. If his mortgage holder couldn’t prove it held his mortgage, it couldn’t foreclose.

Eight years after defaulting, Lents still hasn’t made a payment or been forced out of his house. DLJ, whose parent, Credit Suisse Group AG, declined to comment for this story, still hasn’t proved its ownership to the satisfaction of the court. Lents’s debt has grown to about $2.5 million, including unpaid taxes, interest and penalties.

The Lents Defense

As the stalemate grinds on, Lents has the comfort of knowing he’s no longer alone. When he began demanding to see the IOU, he says, “I was looked upon like I had leprosy. Now, I have probably 20 to 30 people a month come to me” asking for advice. Lents is irked when people accuse him of exploiting a loophole. “It’s not a loophole,” he says. “It’s the law.”

The Lents Defense, as it might be called, doesn’t work everywhere. Thousands of Floridians have lost their homes in lightning-fast “rocket dockets.” In 27 other states, judges don’t even review foreclosures, making it harder for homeowners to fight back. Now, allegations of carelessness and outright fraud in foreclosures have become so widespread that attorneys general in all 50 states are investigating. So are the feds.

Even if the documentation problems turn out to be manageable -- as Bank of America Corp. and others insist they will be -- the economy will still suffer long-term consequences from the loose underwriting that caused the subprime-housing bubble.

$1.1 Trillion

According to an Oct. 15 report by JPMorgan Chase & Co.’s securities unit, some $2 trillion of the $6 trillion in U.S. mortgages and home-equity loans that were securitized during the height of the bubble, from 2005 through 2007, are likely to go into default. The report says the housing bust will ultimately cause losses of $1.1 trillion on those bonds.

While banks and investors take their hits, millions of homeowners continue to be punished by unaffordable mortgage payments and underwater home values. Laurie Goodman, a mortgage analyst at Amherst Securities Group LP in New York, said in an Oct. 1 report that if government doesn’t step up its intervention, more than 11 million borrowers are in danger of losing their homes. That’s one in five people with a mortgage.

“Politically,” she wrote, “this cannot happen. The government will attempt successive modification plans until something works.”

Fight Over Losses

Wall Street’s unspoken strategy has been to kick mortgage losses down the road until an economic recovery reinflates the housing market. The faulty-foreclosure crisis has forced the issue back into the present tense, triggering a fight over who will bear the brunt of those losses. The list of combatants -- all of whom are trying to minimize their share of the damage -- is long: homeowners, lenders and mortgage brokers, loan servicers, underwriters of mortgage-backed securities and buyers of those securities, title insurers, ratings firms, and the federally controlled mortgage buyers Fannie Mae and Freddie Mac.

While JPMorgan predicts that bondholders will absorb most of the estimated $1.1 trillion loss, they may succeed in foisting about $55 billion on banks. If the bank losses turn out to be steeper than JPMorgan and most other analysts expect, taxpayers may be asked to inject more capital into the financial institutions. Fannie Mae and Freddie Mac, already wards of the state, might require more capital as well, the Federal Housing Finance Agency said in an Oct. 21 report.

Careless Lending, Recordkeeping

The past five years of rising foreclosures, to the highest rate since the Great Depression, have exposed the carelessness with which banks lent money. The banks figured they could always seize ownership and resell at a profit, assuming they hadn’t already dumped the loan on an unwary investor. And they wouldn’t let technicalities impede the process. The website 4closurefraud.com, which is operated by the Carol C. Asbury Save My Home Law Group, has links to documents from Nassau County, New York, in which someone entered “BOGUS” as the grantee for the mortgage, or the party entitled to foreclose.

During the housing boom, transactions were flowing so fast that banks couldn’t keep up with the paperwork. The mortgage industry depended on a digital overlay of its own invention, Mortgage Electronic Registration Systems, a database whose owners include Fannie Mae, Freddie Mac, Bank of America, Citigroup Inc.’s CitiMortgage, JPMorgan’s Chase Home Mortgage, Wells Fargo & Co. and title insurers. No matter who bought the loan, MERS was purported to be the mortgagee, or party that would foreclose if a borrower stopped paying.

Assault on the System

Of all newly issued U.S. mortgages, 60 percent list MERS -- a unit of Reston, Virginia-based MERSCorp that has no employees of its own -- as the mortgagee.

“It’s a total attack on the public system,” says Christopher L. Peterson, a law professor at the University of Utah in Salt Lake City who has consulted in cases against MERS.

As MERS sped up loan processing, it created a giant legal hairball. According to Peterson, state judges in Kansas, Arkansas and Maine have said that MERS has no standing in foreclosure proceedings under their states’ laws if they can’t produce the promissory note. In early October, a federal judge in Oregon blocked Bank of America as trustee from foreclosing on a home in the MERS system.

Karmela Lejarde, a MERS spokeswoman, says its standing has always been upheld, “either in the initial court proceeding or upon appeal.”

Judges also resent that would-be foreclosers show up in court representing themselves as vice presidents of MERS even though they work for various loan servicers. Fixing the paperwork won’t be easy because many of the notes have been lost or even deliberately shredded.

Documents Destroyed

The Florida Bankers Association told the state Supreme Court last year that in many cases “the physical document was deliberately eliminated to avoid confusion immediately upon its conversion to an electronic file.”

Beyond the losses to banks, investors and homeowners from the housing crisis, there is an incalculable psychic cost of a legal system that may well have let banks skirt the law.

“The whole financial system is becoming a lot less transparent,” says Hernando de Soto, a Peruvian economist who has written on the importance of well-defined property rights. “You can’t size up risk anymore.”

It’s a perfect October day on the Jacksonville, Florida, campus of Lender Processing Services Inc., and Greg Whitworth, a division president, is rallying a crowd of 200 employees inside a big white tent on the sun-drenched banks of the St. Johns River.

Year of the Megas

“We are killing our competition!” Whitworth says. The company is celebrating what it calls “the Year of the Megas” -- key customers Bank of America, Wells Fargo and JPMorgan Chase -- with a picnic of Mediterranean chicken salad, lemon cooler cookies and sweet tea.

LPS, as the company is known, is the biggest U.S. mortgage- and-foreclosure outsourcing firm. Last year its revenue from default services climbed to $1.1 billion. Its nearest rival, Santa Ana, California-based CoreLogic Inc., takes in less than half of that.

One gray patch hovers over the celebration: The back-office technology provider’s runaway success means it is tangled up in the foreclosure crisis.

“I was thinking about the dark clouds over the company,” Joe Nackashi, the chief information officer, tells the crowd. “Sure, we have made mistakes. But I don’t want to let that cloud this day.”

Plumbing Breaks

LPS supplies much of the digital plumbing for the convoluted home-finance system. At the start of 2010, it said its computer programs were handling 28 million loans with a total principal balance of more than $4.7 trillion -- or more than half the nation’s outstanding mortgage balances. With 8,900 employees and revenue of $2.4 billion, it sells software and manpower to most of the largest U.S. lenders and loan servicers.

“The banks were not prepared for this volume of foreclosures, and that has played to the company’s advantage as the outsourcer,” says Brett Horn, associate director of equity research at Chicago-based Morningstar Inc.

The industry uses LPS computer programs and sometimes LPS employees to code, store and transfer many mortgage records. When things work smoothly, mortgage servicers rely on LPS software to help monitor payments. When homeowners fall behind, LPS helps assemble the information needed to foreclose.

Assembly Line

As described in an in-house newsletter published in September 2006 by Fidelity National Foreclosure Solutions, a predecessor of LPS, a single 18-person “document execution” team brings Henry Ford’s mass-production techniques to the foreclosure business.

“The document execution team is set up like a production line, ensuring that each document request is resolved within 24 hours,” the newsletter said. “On average, the team will execute 1,000 documents per day.”

That was four years ago, when the foreclosure rate was a quarter what it is now. It was when some of those documents proved difficult to track down that trouble set in. If a foreclosure lawyer working on behalf of a bank or servicer asked LPS for an errant mortgage, some company workers may have gone to extremes to keep the foreclosure assembly line moving, according to prosecutors and plaintiffs’ lawyers. The Florida attorney general’s office has alleged that in some cases, corners may have been cut, signatures forged and documents backdated. Industry employees have said in sworn depositions that “robo-signers” executed paperwork without reviewing it.

Florida Investigation

The U.S. Attorney’s Office in Tampa and the state of Florida are investigating whether LPS and affiliated companies have fabricated documents and faked signatures. LPS employees “seem to be creating and manufacturing ‘bogus assignments’ of mortgage in order that foreclosures may go through more quickly and efficiently,” the Florida Attorney General’s Office says in an online description of its civil investigation. “We’re concerned that people might be put out of their houses unfairly and unjustly,” Bill McCollum, the attorney general, told Bloomberg Businessweek.

In a third investigation, the U.S. Trustee Program, the branch of the Justice Department that polices bankruptcies, is looking into whether LPS is “improperly directing legal action” to hasten foreclosures, according to a 2009 opinion issued by the bankruptcy court in Philadelphia. A Trustee spokeswoman declined to comment.

“The system is so organized that there is a company, Lender Processing Services, who allegedly has created the means to systemize fraud,” U.S. Representative Alan Grayson, a Florida Democrat, said Sept. 29, on the House.

Fee Splitting

Foreclosure-defense lawyers have filed suit against LPS in Mississippi and Kentucky, seeking class-action status and accusing the company of improperly splitting fees with pro- foreclosure lawyers. LPS fell 33 percent this year through yesterday in New York Stock Exchange composite trading. That compares with the 12 percent increase by the Standard & Poor’s 400 Midcap Index.

LPS executives acknowledge slip-ups, but nothing amounting to fraud. In a federal securities filing in February, the company said it had “identified a business process that caused an error in the notarization of certain documents, some of which were used in foreclosure proceedings.” LPS says it fixed the problem and closed the subsidiary in Georgia where it occurred.

As for the processing team described in the in-house newsletter, Michelle Kersch, an LPS spokeswoman, says the company decided such affidavit-execution services were “not an appropriate use of resources,” and ended them in September 2008. Still, LPS “signs a limited number of documents for clients,” including assignments of mortgage, she said.

Isolated Errors

“We are dealing with sensationalism versus facts,” Jeffrey S. Carbiener, the company’s chief executive officer, told analysts in an Oct. 6 conference call. “Isolated instances of errors” are bound to occur, but they “are now being brought out and pointed back to that robo-signing, making it sound like a large percentage of these transactions are invalid. That is just simply not the case.” He called the class-action suits “fishing expeditions.”

To keep the paperwork moving, LPS uses a variety of incentives. Top-performing workers receive monthly “Drive for Pride” awards that sometimes include $500 in company stock and a spot in an underground parking garage. LPS also devised a coding system to grade outside foreclosure attorneys based on their speed in completing tasks. Fast-acting attorneys receive green ratings; slower lawyers are labeled yellow or red and may receive fewer assignments.

Fidelity National

“Bill will move quickly and expect you to be there to pull your weight,” says Jerry Mallot, executive vice president of the Jacksonville Regional Chamber of Commerce. “I wouldn’t call the environment at his company kind and genteel.”

Bill is William P. Foley II, a 65-year-old West Point graduate, real estate lawyer and wealthy vintner. He made a fortune assembling the country’s largest title-insurance company, beginning with his purchase in 1984 of Fidelity National Title. By 2003, Fidelity National, then based in Santa Barbara, California, had $10 billion in annual revenue and 32 percent of the U.S. title-insurance market. Frustrated by the high cost of operating in California, Foley was convinced by Mallot and then-Florida Governor Jeb Bush, an occasional golfing companion, to relocate to Jacksonville. A spokeswoman said Foley, who left the LPS board last year, wasn’t available to comment.

Growing Dismay

Spun off in 2008, LPS is one of the city’s largest employers, with 2,400 local workers. Its headquarters is in a 12-story office building on palm-lined Riverside Avenue, part of a complex that also houses Fidelity National Financial, the original title insurer, and Fidelity National Information Services, a 2006 spinoff now called FIS.

Foley and his wife, Carol, split time between a home in Jacksonville’s Ponte Vedra Beach, a ranch in Whitefish, Montana, and California, where Foley owns seven wineries. His compensation last year from LPS and the Fidelity National companies was $45.9 million, according to company filings.

The growth of LPS and other foreclosure outsourcing has dismayed even some professionals deeply involved in the process. Judge Diane Weiss Sigmund of the U.S. Bankruptcy Court in Philadelphia last year published an unusual 58-page opinion scrutinizing LPS because, she said, she wished “to share my education” with others in the system “who may be similarly unfamiliar with the extent that a third-party intermediary drives the Chapter 13 process.”

‘Slavish Adherence’

Her opinion described an attempt by the multinational bank HSBC Holdings Plc to foreclose on the home of Niles and Angela Taylor, who had filed for bankruptcy protection from their creditors. Judge Sigmund ruled the bank’s outside attorneys mistakenly tried to take the Taylors’ home because of three disputed flood-insurance payments totaling $540. She blamed lawyer incompetence, exacerbated by a “slavish adherence” to an LPS computer system called NewTrak.

What bothered the judge, she wrote, was the way HSBC and its lawyers entrusted “the NewTrak system [with] the management of its defaulted loans in bankruptcy. ... With the HSBC data uploaded to an LPS system, LPS responds to the perceived needs of retained counsel. ... The retained counsel does not address the client directly.”

Overreliance on LPS contributed to six months of unnecessary hearings, the judge wrote. After she ordered the parties to settle the issue in person, they did so in just an hour. HSBC acknowledged that the property didn’t require flood insurance after all, and the truce cleared the way for resolution of the Taylors’ bankruptcy plan.

No Punishment

Judge Sigmund, who has since retired, scolded one of HSBC’s outside lawyers for being too “enmeshed in the assembly line” of managing foreclosures and ordered her to take extra ethics training. The judge instructed HSBC to remind all of its lawyers in writing not to defer excessively to computerized data systems. LPS, the judge added, didn’t deserve punishment because the outsourcer had merely provided tools that others misused.

McCollum, the Florida attorney general, suspects that in other cases LPS is more than an innocent facilitator. In April, he says a homeowner contacted his office, alleging that LPS paperwork had been “forged in some way.” His office opened a civil investigation. While McCollum, a Republican, would not provide specifics, subpoenas his office issued on Oct. 13 demand information on six employees of an LPS subsidiary called Docx.

Multiple Titles

The attorney general’s office is investigating whether the employees had the authority to execute mortgage documents for lenders and servicers. One employee, Linda Green, at various times identified herself as a vice president or representative of more than a dozen different banks and mortgage companies, according to the subpoena.

“Docx has produced numerous documents, called assignments of mortgage, that even to the untrained eye appear to be forged and/or fabricated as the signatures of the same individual vary wildly from document to document,” the attorney general’s office says on its website.

LPS disclosed in February that the Tampa U.S. Attorney’s Office is “reviewing the business processes” of the Docx unit. April Charney, a senior attorney with Jacksonville Area Legal Aid and an outspoken critic of LPS, says she was contacted by a federal prosecutor about the company earlier this year. The prosecutor informed her in April, she adds, that the Justice Department was seeking depositions from LPS and Docx employees.

LPS says it shut the Docx unit in April and is cooperating with investigators.

Good for Business

“We feel like we have taken all appropriate corrective actions,” Carbiener, the CEO, told analysts on Oct. 6. “We don’t feel like this is going to have or will have a material impact on our financial results.”

The foreclosure chaos could be good for business, he said. Dogged by foreclosure-defense attorneys and government investigations, lenders and servicers will have to retrace their steps.

“Those services that we provided initially we’ll provide again,” Carbiener said. “For those loans that are held in review, we have the opportunity to earn additional revenues.”

The big banks continue to insist that documentation problems are the legal equivalent of rounding errors.

On Oct. 18, Bank of America, which suspended foreclosures in all 50 states, played down that suspension and said it would resubmit foreclosure affidavits in 23 states after completing a speedy review of 102,000 files. Citigroup said its foreclosure process was “sound.”

‘Blip’

JPMorgan Chase Chief Executive Officer Jamie Dimon told investors on Oct. 13, “If you’re talking about three or four weeks, it will be a blip in the housing market.” He added, “If it went on for a long period of time, it will have a lot of consequences, most of which will be adverse on everybody.”

Ohio Attorney General Richard Cordray on Oct. 19 expressed deep skepticism that Bank of America had managed to complete its internal review in just 2 1/2 weeks, saying, “I would caution that they still have significant financial exposure in many, many cases.”

Even if the homeowners deserve to be foreclosed on, paperwork problems could stand in the way. Mark J. Grant, a managing director for structured finance at Dallas-based Southwest Securities, wrote on Oct. 18 that what may lie ahead is a “Whangdepootenawah,” a word from Ambrose Bierce’s Devil’s Dictionary meaning “disaster; an unexpected affliction that strikes hard.”

‘Retching in the Streets’

Grant wrote, “I doubt that you have followed the contagion down the path to the end because if you had, if anyone had ... there would be a lot more retching in the streets and on Wall Street’s trading desks.”

Even if the IOUs can be straightened out quickly, the fighting won’t stop. Quoting unnamed sources, the Washington Post reported on Oct. 19 that the Obama administration’s Financial Fraud Enforcement Task Force is investigating whether financial firms committed federal crimes in filing fraudulent court documents to seize people’s homes.

Meanwhile, a high-stakes fight is breaking out between the banks that made loans and the investors who bought them. A shot was fired on Oct. 18 when a group of major investors claimed that Bank of America’s Countrywide Home Loan Servicing had failed to live up to its contracts on some of more than $47 billion worth of Countrywide-issued mortgage bonds. The group said Countrywide Servicing has 60 days to correct the alleged violations, such as failure to sell back ineligible loans to the lenders. According to people familiar with the matter, the group includes Pacific Investment Management Co., BlackRock Inc. and the Federal Reserve Bank of New York.

Loss Estimates

For banks that have just started making money again after near-death experiences in 2008, mortgage losses could delay the return to good health. Chris Gamaitoni, an analyst for Compass Point Research & Trading, a Washington financial advisory firm, estimates losses for the big banks of $134 billion from having to buy back bad loans from private investors and another $27 billion in losses from buying back loans from Fannie Mae and Freddie Mac. Other estimates are lower--from $20 billion to $84 billion--in part because those analysts are less certain than Gamaitoni that investors will succeed in court.

Bank of America, the nation’s largest lender, has resorted to tough tactics in resisting repurchases of bad loans. Facing pressure from Freddie Mac, one of the two government-controlled mortgage-finance companies, to buy back money-losing home loans with problems like inflated appraisals, overstated borrower income, or inadequate documentation, Bank of America issued a blunt threat, according to two people with direct knowledge of the incident.

Never in Writing

If Freddie Mac didn’t back off its demands for the buybacks, Bank of America officials said, the bank would take more of the new, more profitable mortgages it is originating these days to rival Fannie Mae, these people said. Freddie and Fannie, known as GSEs for government-sponsored entities, need a steady supply of healthy new loans to climb out of their financial hole.

The claimed threat from Bank of America, which wasn’t put into writing, according to one of these people, was taken seriously enough that it has been discussed at several Freddie Mac board meetings, including in mid-October. Some officials have urged the Federal Housing Finance Agency -- the government conservator that has controlled Fannie and Freddie since they were bailed out in 2008 -- to confront Bank of America and prevent it from trying to play one against the other, which may be infuriating but is not illegal.

The Dilemma

“If the tactic worked, I’d be shocked and appalled,” said Thomas Lawler, a former portfolio manager at Fannie Mae and now an economic consultant. “The GSEs are supposed to be run now to minimize losses to the taxpayers. Freddie ought to ignore the threat.”

FHFA Acting Director Edward J. DeMarco declined to comment, as did officials of Freddie Mac. Bank of America, based in Charlotte, North Carolina, also declined to comment.

For policy makers, the dilemma is this: Enormous losses will cause problems wherever they end up. They could further harm Fannie and Freddie, which insure the vast majority of the nation’s mortgages and have already received almost $150 billion in taxpayer support. Or, if Fannie and Freddie succeed in pushing the burden back to the banks, the losses could cripple some of the major institutions that have just emerged from a government bailout.

Buyback Requests

Bank of America faces $12.9 billion in buyback requests, and mortgage insurers have asked for the documents on an additional $9.8 billion on which they may consider seeking repurchases, according to regulatory filings. Bank of America has put aside $4.4 billion for buybacks, and CEO Brian T. Moynihan says the costs will be manageable.

“The Treasury is very aware that they can’t push too hard on this because if you do push too hard it might put the companies in negative capital again,” says Paul J. Miller, an analyst at FRB Capital Markets in Arlington, Virginia. “There’s a lot of regulatory forbearance going on.”

Aside from ignoring banks’ bad debts, the federal government hasn’t done much to fix the crisis. Both houses of Congress easily passed a bill this year that would have undermined centuries of law by requiring every state to recognize MERS-type electronic records from other states. Only a pocket veto by President Barack Obama kept it from becoming law.

One option, opposed by Obama and most Republicans in Congress but favored by Senate Majority Leader Harry Reid and others, is a national moratorium on foreclosures. It would last until regulators assure themselves that lenders have straightened out their foreclosure procedures.

Proposals

Opponents say it would delay the recovery of the housing market by preventing qualified buyers from getting their hands on foreclosed homes. Supporters of the idea, such as Dean Baker, co-director of the Center for Economic and Policy Research in Washington, say there are plenty of already foreclosed homes available for sale and thus no urgent need to add to the supply.

Goodman, the Amherst Securities analyst, says banks need to reduce the principal that people owe on their homes so they have an incentive not to walk away. “Ignoring the fact that the borrower can and will default when it is his/her most economical solution is an expensive case of denial,” Goodman writes. If the home whose mortgage was reduced happens to regain value, 50 percent of the appreciation would be taxed, she says. Meanwhile, to discourage people from sitting tight in homes while foreclosure proceedings drag on, she would have the government tax the benefit of living in the home rent-free.

Speed Is Needed

CitiMortgage is testing an innovative alternative based on the legal procedure known as “deed in lieu of foreclosure.” The owner turns the deed over to the bank without a fight if the bank promises not to foreclose, lets the family stay in the house after the agreement for six months and gives relocation assistance.

In a New York Times blog post on Oct. 19, Harvard University economist Edward Glaeser suggested federal assistance to overwhelmed state and local courts, as well as $2,000 vouchers for legal assistance to low-income families that can’t afford to fight foreclosures. Bloomberg News columnist Kevin Hassett, who is director of economic policy studies at the American Enterprise Institute in Washington, wrote in his Oct. 18 column that the newly created Financial Stability Oversight Council should make the foreclosure mess its first big project, “take authority for solving it, and do so as swiftly as possible.”

Speed is essential. The longer it drags on, the more the foreclosure crisis corrodes Americans’ faith in their financial and legal systems. A pervasive sense of injustice is bad for the economy and democracy as well. Take Joe Lents. The Boca Raton homeowner hasn’t made a mortgage payment since 2002, but he perceives himself as a victim. “I want to expose these guys for what they’re doing,” Lents says. “It’s personal now.”

URL to original article: http://www.housingwire.com/2010/10/21/how-joseph-lents-dodged-foreclosure-for-eight-years-and-started-a-movement

In 2002, an accountant in Boca Raton, Florida, named Joseph Lents was accused of securities-law violations by the U.S. Securities and Exchange Commission. Lents, who was chief executive officer of a now-defunct voice- recognition software company, had sold shares in the public company without filing the proper forms. Facing a little over $100,000 in fines and fees, and with his assets frozen by the SEC, Lents stopped making payments on his $1.5 million mortgage.

The loan servicer, Washington Mutual Inc., tried to foreclose on his home in 2003 but was never able to produce Lents’s promissory note, so the state circuit court for Palm Beach County dismissed the case. Next, the buyer of the loan, DLJ Mortgage Capital, stepped in with another foreclosure proceeding. DLJ claimed to have lost the promissory note in interoffice mail. Lents was dubious.

“When you say you lose a $1.5 million negotiable instrument -- that doesn’t happen,” he said in an interview in Bloomberg Businessweek’s Oct. 25 issue.

DLJ claimed that its word was as good as paper. But at least in Palm Beach County, paper still rules. If his mortgage holder couldn’t prove it held his mortgage, it couldn’t foreclose.

Eight years after defaulting, Lents still hasn’t made a payment or been forced out of his house. DLJ, whose parent, Credit Suisse Group AG, declined to comment for this story, still hasn’t proved its ownership to the satisfaction of the court. Lents’s debt has grown to about $2.5 million, including unpaid taxes, interest and penalties.

The Lents Defense

As the stalemate grinds on, Lents has the comfort of knowing he’s no longer alone. When he began demanding to see the IOU, he says, “I was looked upon like I had leprosy. Now, I have probably 20 to 30 people a month come to me” asking for advice. Lents is irked when people accuse him of exploiting a loophole. “It’s not a loophole,” he says. “It’s the law.”

The Lents Defense, as it might be called, doesn’t work everywhere. Thousands of Floridians have lost their homes in lightning-fast “rocket dockets.” In 27 other states, judges don’t even review foreclosures, making it harder for homeowners to fight back. Now, allegations of carelessness and outright fraud in foreclosures have become so widespread that attorneys general in all 50 states are investigating. So are the feds.

Even if the documentation problems turn out to be manageable -- as Bank of America Corp. and others insist they will be -- the economy will still suffer long-term consequences from the loose underwriting that caused the subprime-housing bubble.

$1.1 Trillion

According to an Oct. 15 report by JPMorgan Chase & Co.’s securities unit, some $2 trillion of the $6 trillion in U.S. mortgages and home-equity loans that were securitized during the height of the bubble, from 2005 through 2007, are likely to go into default. The report says the housing bust will ultimately cause losses of $1.1 trillion on those bonds.

While banks and investors take their hits, millions of homeowners continue to be punished by unaffordable mortgage payments and underwater home values. Laurie Goodman, a mortgage analyst at Amherst Securities Group LP in New York, said in an Oct. 1 report that if government doesn’t step up its intervention, more than 11 million borrowers are in danger of losing their homes. That’s one in five people with a mortgage.

“Politically,” she wrote, “this cannot happen. The government will attempt successive modification plans until something works.”

Fight Over Losses

Wall Street’s unspoken strategy has been to kick mortgage losses down the road until an economic recovery reinflates the housing market. The faulty-foreclosure crisis has forced the issue back into the present tense, triggering a fight over who will bear the brunt of those losses. The list of combatants -- all of whom are trying to minimize their share of the damage -- is long: homeowners, lenders and mortgage brokers, loan servicers, underwriters of mortgage-backed securities and buyers of those securities, title insurers, ratings firms, and the federally controlled mortgage buyers Fannie Mae and Freddie Mac.

While JPMorgan predicts that bondholders will absorb most of the estimated $1.1 trillion loss, they may succeed in foisting about $55 billion on banks. If the bank losses turn out to be steeper than JPMorgan and most other analysts expect, taxpayers may be asked to inject more capital into the financial institutions. Fannie Mae and Freddie Mac, already wards of the state, might require more capital as well, the Federal Housing Finance Agency said in an Oct. 21 report.

Careless Lending, Recordkeeping

The past five years of rising foreclosures, to the highest rate since the Great Depression, have exposed the carelessness with which banks lent money. The banks figured they could always seize ownership and resell at a profit, assuming they hadn’t already dumped the loan on an unwary investor. And they wouldn’t let technicalities impede the process. The website 4closurefraud.com, which is operated by the Carol C. Asbury Save My Home Law Group, has links to documents from Nassau County, New York, in which someone entered “BOGUS” as the grantee for the mortgage, or the party entitled to foreclose.

During the housing boom, transactions were flowing so fast that banks couldn’t keep up with the paperwork. The mortgage industry depended on a digital overlay of its own invention, Mortgage Electronic Registration Systems, a database whose owners include Fannie Mae, Freddie Mac, Bank of America, Citigroup Inc.’s CitiMortgage, JPMorgan’s Chase Home Mortgage, Wells Fargo & Co. and title insurers. No matter who bought the loan, MERS was purported to be the mortgagee, or party that would foreclose if a borrower stopped paying.

Assault on the System

Of all newly issued U.S. mortgages, 60 percent list MERS -- a unit of Reston, Virginia-based MERSCorp that has no employees of its own -- as the mortgagee.

“It’s a total attack on the public system,” says Christopher L. Peterson, a law professor at the University of Utah in Salt Lake City who has consulted in cases against MERS.

As MERS sped up loan processing, it created a giant legal hairball. According to Peterson, state judges in Kansas, Arkansas and Maine have said that MERS has no standing in foreclosure proceedings under their states’ laws if they can’t produce the promissory note. In early October, a federal judge in Oregon blocked Bank of America as trustee from foreclosing on a home in the MERS system.

Karmela Lejarde, a MERS spokeswoman, says its standing has always been upheld, “either in the initial court proceeding or upon appeal.”

Judges also resent that would-be foreclosers show up in court representing themselves as vice presidents of MERS even though they work for various loan servicers. Fixing the paperwork won’t be easy because many of the notes have been lost or even deliberately shredded.

Documents Destroyed

The Florida Bankers Association told the state Supreme Court last year that in many cases “the physical document was deliberately eliminated to avoid confusion immediately upon its conversion to an electronic file.”

Beyond the losses to banks, investors and homeowners from the housing crisis, there is an incalculable psychic cost of a legal system that may well have let banks skirt the law.

“The whole financial system is becoming a lot less transparent,” says Hernando de Soto, a Peruvian economist who has written on the importance of well-defined property rights. “You can’t size up risk anymore.”

It’s a perfect October day on the Jacksonville, Florida, campus of Lender Processing Services Inc., and Greg Whitworth, a division president, is rallying a crowd of 200 employees inside a big white tent on the sun-drenched banks of the St. Johns River.

Year of the Megas

“We are killing our competition!” Whitworth says. The company is celebrating what it calls “the Year of the Megas” -- key customers Bank of America, Wells Fargo and JPMorgan Chase -- with a picnic of Mediterranean chicken salad, lemon cooler cookies and sweet tea.

LPS, as the company is known, is the biggest U.S. mortgage- and-foreclosure outsourcing firm. Last year its revenue from default services climbed to $1.1 billion. Its nearest rival, Santa Ana, California-based CoreLogic Inc., takes in less than half of that.

One gray patch hovers over the celebration: The back-office technology provider’s runaway success means it is tangled up in the foreclosure crisis.

“I was thinking about the dark clouds over the company,” Joe Nackashi, the chief information officer, tells the crowd. “Sure, we have made mistakes. But I don’t want to let that cloud this day.”

Plumbing Breaks

LPS supplies much of the digital plumbing for the convoluted home-finance system. At the start of 2010, it said its computer programs were handling 28 million loans with a total principal balance of more than $4.7 trillion -- or more than half the nation’s outstanding mortgage balances. With 8,900 employees and revenue of $2.4 billion, it sells software and manpower to most of the largest U.S. lenders and loan servicers.

“The banks were not prepared for this volume of foreclosures, and that has played to the company’s advantage as the outsourcer,” says Brett Horn, associate director of equity research at Chicago-based Morningstar Inc.

The industry uses LPS computer programs and sometimes LPS employees to code, store and transfer many mortgage records. When things work smoothly, mortgage servicers rely on LPS software to help monitor payments. When homeowners fall behind, LPS helps assemble the information needed to foreclose.

Assembly Line

As described in an in-house newsletter published in September 2006 by Fidelity National Foreclosure Solutions, a predecessor of LPS, a single 18-person “document execution” team brings Henry Ford’s mass-production techniques to the foreclosure business.

“The document execution team is set up like a production line, ensuring that each document request is resolved within 24 hours,” the newsletter said. “On average, the team will execute 1,000 documents per day.”

That was four years ago, when the foreclosure rate was a quarter what it is now. It was when some of those documents proved difficult to track down that trouble set in. If a foreclosure lawyer working on behalf of a bank or servicer asked LPS for an errant mortgage, some company workers may have gone to extremes to keep the foreclosure assembly line moving, according to prosecutors and plaintiffs’ lawyers. The Florida attorney general’s office has alleged that in some cases, corners may have been cut, signatures forged and documents backdated. Industry employees have said in sworn depositions that “robo-signers” executed paperwork without reviewing it.

Florida Investigation

The U.S. Attorney’s Office in Tampa and the state of Florida are investigating whether LPS and affiliated companies have fabricated documents and faked signatures. LPS employees “seem to be creating and manufacturing ‘bogus assignments’ of mortgage in order that foreclosures may go through more quickly and efficiently,” the Florida Attorney General’s Office says in an online description of its civil investigation. “We’re concerned that people might be put out of their houses unfairly and unjustly,” Bill McCollum, the attorney general, told Bloomberg Businessweek.

In a third investigation, the U.S. Trustee Program, the branch of the Justice Department that polices bankruptcies, is looking into whether LPS is “improperly directing legal action” to hasten foreclosures, according to a 2009 opinion issued by the bankruptcy court in Philadelphia. A Trustee spokeswoman declined to comment.

“The system is so organized that there is a company, Lender Processing Services, who allegedly has created the means to systemize fraud,” U.S. Representative Alan Grayson, a Florida Democrat, said Sept. 29, on the House.

Fee Splitting

Foreclosure-defense lawyers have filed suit against LPS in Mississippi and Kentucky, seeking class-action status and accusing the company of improperly splitting fees with pro- foreclosure lawyers. LPS fell 33 percent this year through yesterday in New York Stock Exchange composite trading. That compares with the 12 percent increase by the Standard & Poor’s 400 Midcap Index.

LPS executives acknowledge slip-ups, but nothing amounting to fraud. In a federal securities filing in February, the company said it had “identified a business process that caused an error in the notarization of certain documents, some of which were used in foreclosure proceedings.” LPS says it fixed the problem and closed the subsidiary in Georgia where it occurred.

As for the processing team described in the in-house newsletter, Michelle Kersch, an LPS spokeswoman, says the company decided such affidavit-execution services were “not an appropriate use of resources,” and ended them in September 2008. Still, LPS “signs a limited number of documents for clients,” including assignments of mortgage, she said.

Isolated Errors

“We are dealing with sensationalism versus facts,” Jeffrey S. Carbiener, the company’s chief executive officer, told analysts in an Oct. 6 conference call. “Isolated instances of errors” are bound to occur, but they “are now being brought out and pointed back to that robo-signing, making it sound like a large percentage of these transactions are invalid. That is just simply not the case.” He called the class-action suits “fishing expeditions.”

To keep the paperwork moving, LPS uses a variety of incentives. Top-performing workers receive monthly “Drive for Pride” awards that sometimes include $500 in company stock and a spot in an underground parking garage. LPS also devised a coding system to grade outside foreclosure attorneys based on their speed in completing tasks. Fast-acting attorneys receive green ratings; slower lawyers are labeled yellow or red and may receive fewer assignments.

Fidelity National

“Bill will move quickly and expect you to be there to pull your weight,” says Jerry Mallot, executive vice president of the Jacksonville Regional Chamber of Commerce. “I wouldn’t call the environment at his company kind and genteel.”

Bill is William P. Foley II, a 65-year-old West Point graduate, real estate lawyer and wealthy vintner. He made a fortune assembling the country’s largest title-insurance company, beginning with his purchase in 1984 of Fidelity National Title. By 2003, Fidelity National, then based in Santa Barbara, California, had $10 billion in annual revenue and 32 percent of the U.S. title-insurance market. Frustrated by the high cost of operating in California, Foley was convinced by Mallot and then-Florida Governor Jeb Bush, an occasional golfing companion, to relocate to Jacksonville. A spokeswoman said Foley, who left the LPS board last year, wasn’t available to comment.

Growing Dismay

Spun off in 2008, LPS is one of the city’s largest employers, with 2,400 local workers. Its headquarters is in a 12-story office building on palm-lined Riverside Avenue, part of a complex that also houses Fidelity National Financial, the original title insurer, and Fidelity National Information Services, a 2006 spinoff now called FIS.

Foley and his wife, Carol, split time between a home in Jacksonville’s Ponte Vedra Beach, a ranch in Whitefish, Montana, and California, where Foley owns seven wineries. His compensation last year from LPS and the Fidelity National companies was $45.9 million, according to company filings.

The growth of LPS and other foreclosure outsourcing has dismayed even some professionals deeply involved in the process. Judge Diane Weiss Sigmund of the U.S. Bankruptcy Court in Philadelphia last year published an unusual 58-page opinion scrutinizing LPS because, she said, she wished “to share my education” with others in the system “who may be similarly unfamiliar with the extent that a third-party intermediary drives the Chapter 13 process.”

‘Slavish Adherence’

Her opinion described an attempt by the multinational bank HSBC Holdings Plc to foreclose on the home of Niles and Angela Taylor, who had filed for bankruptcy protection from their creditors. Judge Sigmund ruled the bank’s outside attorneys mistakenly tried to take the Taylors’ home because of three disputed flood-insurance payments totaling $540. She blamed lawyer incompetence, exacerbated by a “slavish adherence” to an LPS computer system called NewTrak.

What bothered the judge, she wrote, was the way HSBC and its lawyers entrusted “the NewTrak system [with] the management of its defaulted loans in bankruptcy. ... With the HSBC data uploaded to an LPS system, LPS responds to the perceived needs of retained counsel. ... The retained counsel does not address the client directly.”

Overreliance on LPS contributed to six months of unnecessary hearings, the judge wrote. After she ordered the parties to settle the issue in person, they did so in just an hour. HSBC acknowledged that the property didn’t require flood insurance after all, and the truce cleared the way for resolution of the Taylors’ bankruptcy plan.

No Punishment