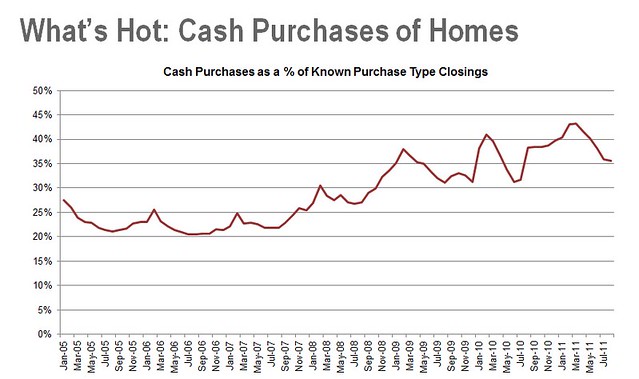

With cash closings skyrocketing, I was curious to find out whether cash transactions were concentrated in any way. So, I asked my HWMI colleague, executive director of research Jonathan Smoke, to take a look at the data for me. So, he took this ...

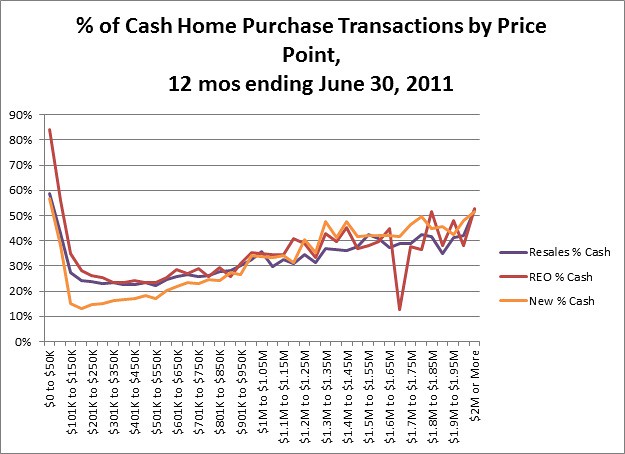

... and broke it down by both housing type--REO, regular resale, and new-home sales--and price point to get this:

Across all three housing segments, the trend is similar: The more expensive the home, the more likely buyers have been to use cash to make the purchase. However, the major exception to the rule is at the other end of the spectrum, where extremely high percentages of all purchases of homes for under $100,000 were cash transactions.

But I want to focus on the new-home piece of this data puzzle for a second.

The fear these days, especially as the industry bids adieu to the higher loan limits for mortgages backed by Fannie Mae and Freddie Mac, as well as those insured by the FHA, is that continuing mortgage constraints will strangle what demand is in the housing market. And post federal home buyer tax credit, that demand has clearly been in the move-up tranche of the new-home market. The reasons are fairly simple. Move-up buyers tend to be more established, so they often have bigger incomes, better credit scores, fewer debts, and can access financing more easily. They also typically have more savings. But is the typical move-up buyer using that cash to make a bigger down payment or is she choosing to bypass financing all together and buying the property outright?

According to HWMI data, 18% of new-home sales were all-cash transactions, compared with 30% or regular resales and 49% of REO sales. I'm not sure if that's surprisingly low or surprisingly high to most builders.

Volumes are definitely low enough right now that having just shy of 1 in 5 sales as cash sales seems like a lot. However, it's definitely at the higher price points--$600,000 and up--where cash becomes a much bigger deal. And then there's clearly an inflection point around the $900,000 mark, where the percentage of all cash transactions for new homes starts to eclipse the rate of such for both regular resales and REO sales.

But how much of the new-home market, or even the move-up piece of that market, is really happening at those price points? Outside select luxury builders or those with a geographic concentration in hyper-expensive areas like coastal California or metro New York, for example--do many traditional production builders really consider those ranges their sweet spot anymore? Given how much prices have reset over the past few years, in some areas it would seem that $450,000 is the new $600,000.

While the new-home market is definitely seeing a shift toward more cash transactions, Smoke said it's important to remember it's still small relative to REO and even regular resales. But it is clearly indicative of financing constraints, he said, especially considering that (1) there's been a decline in the total percent financed and (2) big builder mortgage companies are gaining market share against traditional mortgage lenders.

"The big builders with captive mortgage companies have a clear advantage, assuming that these captives can get the necessary funding or package and resell the mortgages," he said.

So, the bottom line: In a world of cash transactions, financing is still king.

URL to original article: http://www.bigbuilderonline.com/post.asp?BlogId=yaussisblog&postid=662956§ionID=1939&cid=BP:093011:FULL

For further information on Fresno Real Estate check: http://www.londonproperties.com

No comments:

Post a Comment